刚刚结束的联邦预算对中小生意和个人是个利好消息,这篇文章在陈述一些具体的政策细节外会着重分析对中小生意和个人的税务有什么实质性影响。

中小企业

- 资产一次性抵扣税

先看看中小企业的新政策,继2015年以来,政府颁布了$20,000首次使用或安装待用的资产小生意可以在购买当年一次性用来抵扣税的政策,2019年1月29日,政府将资产价格限定额度增长为$25,000,新的预算将从预算当日起即4月2日东部时间7:30pm进一步将该额度增加到$30,000。而且这个额度适用于每个资产,对购买的资产数量没有上限限制。该政策原来只适用于小型企业,即年营业额不超过$1,000万的企业,然而新政策将扩展到年营业额不超过$5000万的中型企业。请看下面列表会有更清晰地认识:

|

2015年5月12日东部时间7:30pm -2019年1月28日资产额度限制 |

2019年1月29日-2019年4月2日东部时间7:30pm资产额度限制 |

2019年4月2日东部时间7:30pm-2020年6月30日资产额度限制 |

| 小型企业(年营业额<$1,000万) |

$20,000 |

$25,000 |

$30,000 |

| 中型企业($1,000<年营业额<$5,000万) |

不适用 |

不适用 |

$30,000 |

从税务角度来说一次性抵扣对中小生意有何影响。打比方说,一个年收入$90,000有ABN的建筑合同工,买了一辆$30,000的车,假设完全用于生意用途并且在年初购买,以前按照标准折旧的方法,一年的车子可以用来抵扣的额度是$3,750 (30,000/8年),但是按照新政策的方法,此合同工可以在购买车当年将$30,000全部用来抵扣,那么政策前后的第一年的抵税额的差别就是$26,250,转换成税上的节省就是$9,056.25 (26250*(32.5%+2% 医保费))(没有考虑低收入抵税等因素)。虽然老的政策原来的折旧会在未来渐渐抵扣完,可是以后的税率可能会降低或是车子完全不再用于生意,再加上现金流折现值的考虑,第一年直接全额抵税自然是首选。对于公司的情况,按照现在公司税率,税务上第一年的节省额度也达到 $7,218.75 (26,250*27.5%)。所以如果你2015年5月12日后,购买的大件资产却没有给你当年减免较多的税,建议可以进行复查。

这里值得一提的是那个扩展到$25,000 和 $30,000的额度现在还没有通过立法,所以安全起见还是先买低于$20,000的资产,等正式立法了再买$30,000的也不迟。

- 增强商业注册号ABN系统

另一个政策是关于要求具有ABN的企业做以下:

- 从2021年7月1日起,每年需要完成他们的税务申报

- 从2022年7月1日起, 每年需要检查他们在ABN注册处的信息准确性

目前,以上两点未完成的企业在短期内仍然可以持有ABN。吊销ABN会立即影响到日常的生意经营,甚至会影响到银行贷款,所以建议用ABN进行贷款的人士,到时注意合规。

- 一键式薪酬系统的拓展

从今年的7月,一键式薪酬系统正式拓展到雇佣人数低于20人的中小企业。该政策对中小企业的影响将是什么呢:

- 没有安装具有一键式薪酬系统功能软件的雇主需要升级或重新购买具有该项功能的软件;

- 员工的工资和养老金系统将在每次发工资时上报给税局,以后迟交的随赚随缴预扣税款和员工养老金将很容易被税局发觉,随之而来的罚款和惩罚将是很昂贵的;

- 以后工资发错,需要在规定的时间内完成纠正,整个纠正过程需要的人力物力可能比现在要多很多

- 延长和加大反逃税力度

政府在未来的四年将拨款10亿澳元给税局坚持贯彻反逃税计划,进一步扩大清查工作和市场覆盖范围,并将该项目延长至2023年。那些通过不合规的国际低税率国家、税务构架和策划等逃税个体将成为审查的重点对象。

个人税务

- 个人所得税

从2022年7月1日起,19%的税率档将由现在的$37,000提升到$45,000,从2024年7月1日起,现在的32.5%的税率档的税率将降到30%,并且将该档由$120,000提升到$200,000。具体变动请看下表:

|

2019财政年 |

2023财政年起 |

2025财政年起 |

| 0% |

0-18,200 |

0-18,200 |

0-18,200 |

| 19% |

18,201-37,000 |

18,201-45,000 |

18,201-45,000 |

| 30% |

|

|

45,001-200,000 |

| 32.5% |

37,001-90,000 |

45,001-120,000 |

|

| 37% |

90,001-180,000 |

12,001-180,000 |

|

| 45% |

180,001+ |

180,001+ |

200,001+ |

就其他条件不变,如果税率档2024年7月1日变动后,和现在的税率相比,一个收入$65,000和$150,000的人的税额将会有何变化,请看下表:

|

2019财政年 |

2025财政年起 |

| 收入$65,000 |

$12,672* |

$11,092* |

| 收入$15,0000 |

$42,997* |

$36,592* |

*以上计算不考虑医保费及低收入和中低收入抵税等因素

从以上的分析看出,新政策对中低收入人群有些许利好,但对中高收入的人群利好会更多一些。从收入$45,000到$200,000征收一样的税率,对于整个税务系统的公平性有待进一步考究。

从税务策划角度来说,以前企业主工资收入基本发到32.5%的$90,000万上限,将来可以发到$200,000了,同样30%税率的被动收入公司和家庭信托的建立和应用可能也会有所减少。

- 中低收入的抵税额变化

目前的中低收入抵税额最高是$530,起步基数是$200,新政策下抵税额将翻一番,达到$1080,起步基数是$255。请看新政策下的抵税额:

| 应税收入 |

抵税额 |

| 0 – 37,000 |

$255 |

| 37,001 – 48, 000 |

$255 + 应税金额超过37,000部分的7.5% |

| 48,001 – 90,000 |

$1,080 |

| 90,001 – 126,000 |

$1,080 – 应税金额超过90,000部分的3% |

| 126,001+ |

0 |

从表格中不难看出,新政策下的抵税金额可以让个人年收入$48,001到$90,000的家庭在税务上可以节省$2,160, 其他年收入区间在$0 – $126,000的个人也可以有$0 – $2,160不等的抵税额。

这个中低收入抵税额从今年这个财政年开始并且是在现有的低收入抵税额 $445基础上额外的抵税额。从2022年开始,中低收入抵税额和低收入抵税额将合并为一个低收入抵税额,最高抵税额度可以达到$700。

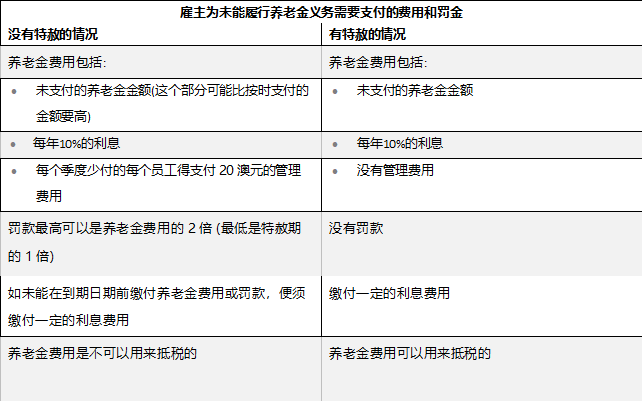

养老金

- 65和66岁工作测试的移除

从2020年7月1日起,65和66岁的人士不需要通过工作测试也可以向自己养老金中主动打入储蓄,目前65-74岁人士都需要满足工作测试才可以这么操作。

- 65和66岁可以享受‘提前规则’

一般来说,一个人一年往养老金中可以打入的非优惠储蓄封顶是$10万。目前只有65岁以下人士才可以利用 ‘提前规则’向自己的养老金,在一年中打入下面三年的允许的总和,即$30万。新政策允许,65和66岁人士也可以利用此规则,并且不用通过工作测试。

- 提高允许配偶养老金储蓄的年龄

新政策允许74岁及以下人士接受配偶养老金储蓄,目前70岁及以上人士是不允许这么操作的。

从以上养老金的新政策可以看出政府是鼓励老龄者及退休人士主动往养老金里打入储蓄,对于政府可以减少公共养老的负担,对于个人从某种程度上可以节省一些储蓄和投资回报的税额,因为养老金里收入的税率只有15%,而年龄65及以上者往往已经退休了,所以他们的养老金的投资回报很多是免税的。

皮特马丁(PittMartin)会计师事务所是一家提供税务,会计,生意咨询及自管养老金综合性服务的经澳洲会计师公会认证的会计师事务所。我们的中文联系方式是 Robert Liu +61292213345或邮件robert@pittmartingroup.com.au。皮特马丁(Pitt Martin)会计师事务所坐落在悉尼市市中心,交通过来非常方便。

本文内容仅供参考,不构成对任何个人或团体的具体情况而形成建议。任何个人或团体应该在征求专业人士的意见后方可采取行动。由于税法的时效性,我们在发布时已致力于提供及时、准确的信息,但不能保证所称述的内容在今后任然可以适用。转发该文内容请注明出处。

Experienced Tax Accountant and Business Advisor with a demonstrated history of working in the accounting and mortgage industry. Skilled in Tax, Accounting, Business Advisory, SMSF, Audit and Mortgage. Strong entrepreneurship professional with qualification Master of Professional Accounting, CA Public Practice, Registered Tax Agent, Registered ASIC Agent, NSW Law Society External Examiner, Trust Account Auditor and Diploma of Finanical Planning. Specialised in SME, tax planning and international tax, he helped client save ample money and create wealth.